Commercial Banks:

Commercial Banks are financial institution who accepts deposits from the public and

provide loans facilities for investment with the aim of earning profit.

Functions of Commercial Banks:-

1. Primary functions:-

(a) Accepting deposits

(b) Advancing loans

2Secondary functions:-

1. Agency function

(a) Transfer of fund

(b) Collection of funds

(c) Purchase and sale of shares and securities on behalf of the customers.

(d) Collection of dividend and interest

(e) Payment of bills and insurance premium on behalf of customers

(f) Acting as executor and trustee of will

(g) Acting as correspondent and representative of customer and provide letter of credit to the customer.

2. General utility function

(a) Purchase and sell of foreign exchange.

(b) Issuance of travelerscheque.

(c) Safe custody of valuable goods in lockers.

(d) Underwriting of securities.

Central Banks:

1.The central Bank is the apex institution of monetary and financial system of a country.

2.It makes monetary policy of the country in public interest.

3.It manages, supervises and facilitates the banking system of the country.

Functions of Central Banks

1. Bank of Issue

2. Banker to the Government

3. Banker’s Bank and Supervisor.

4. Controller of credit.

5. Lender of last resort

6. Custodian of foreign exchange reserves

MONEY CREATION OR CREDIT CREATION BY COMMERCIAL BANKS

CREDIT is defined as finance made available by one party to another party on a certain rate of exchange.

The capacity of banks to create money or credit depends on:-

(i) Amount of primary deposits

(ii) Legal reserve ratio(LRR).

Legal Reserve Ratio(LRR):- is fixed by the central bank of a country and it is the minimum ratio of deposit legally required to be kept as cash by banks.

Cash Reserve Ratio(CRR):- It is a part of LRR which is to be kept with the central bank.

Statutory Liquidity Ratio(SLR):- It is a part of LRR which is to be kept with the bank themselves.

Commercial bank’s demand deposits are a part of money supply. Commercial banks lend money to the borrowers by opening demand deposit account in their names. The borrowers are free to use this money by writing cheques. According to definition demand deposits are a part of money supply. Therefore, by creating additional demand deposits bank create money.

Money creation depends upon two factor:

1. Primary deposits

2. Legal Reserve Ratio (LRR).

Multiplier = 1/LRR Total Deposit creation = Initial deposit X 1/LRR.

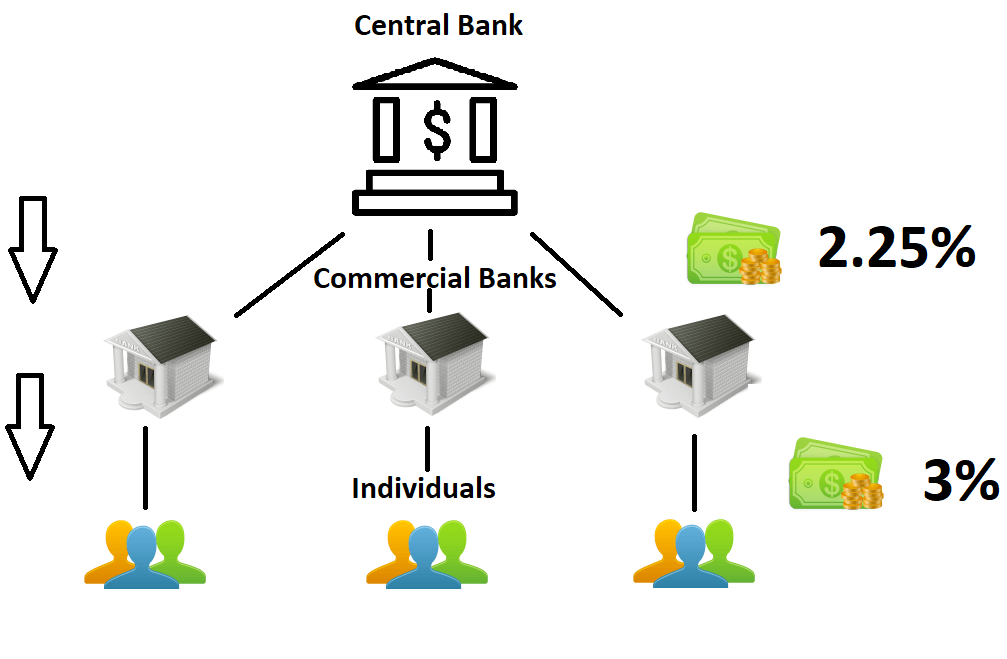

Repo rate : Repo rate is the rate at which the central bank of a country (Reserve Bank of India in case of India) lends money to commercial banks in the event of any shortfall of funds. Repo rate is used by monetary authorities to control inflation.

Reverse repo rate : Reverse repo rate is the rate at which the central bank of a country (Reserve Bank of India in case of India) borrows money from commercial banks within the country. It is a monetary policy instrument which can be used to control the money supply in the country.